How to change a successful transparent approach to pricing in an evolving international trade

Business decisions are increasingly driven by the analysis of data on market trends, consumer behaviour, and the purchasing journey. In many companies, management and operational choices now rely more on scientific methods than on the traditional entrepreneur’s instinct, which still plays a role in highly complex situations but is gradually yielding to more analytical, data-oriented thinking. The growing importance of online channels in purchasing, as well as in product search, evaluation, and review, significantly accelerates this transition.

Within the broader landscape of management decisions, pricing still belongs, in most cases, to a largely intuitive “art,” where entrepreneurs metaphorically consult a crystal ball to define their strategy and set price levels. The aim of this article is not to prescribe the exact steps for identifying the perfect price—a kind of modern Holy Grail—but to show how to abandon longstanding habits shaped by decades of management practice and driven by a single guiding objective: pure profit maximization.

This discussion does not concern only “customers,” but the entire set of actors in the supply chain. Managers often seek not just the highest prices the market will bear for their own products and services, but also the lowest possible prices from their suppliers, with the overarching aim of securing the largest possible share of the total value created, whatever the cost. Some managers proactively and systematically deploy all available tools to achieve this goal, while others simply push to increase their share without making it their sole reason for being. In both cases, their behaviour is inspired by the same underlying principle.

In recent years, thanks to an evolving movement that is creating pressure to adopt a more sustainable approach to business, more and more researchers published studies showing the great advantages in setting up the principle of “shared value” among the stakeholders and, in the specific field, the application of “fair pricing” within the overall concept of fairness toward customers and suppliers. The aim of this article is to inspire entrepreneurs to change their approach to this delicate management policy endorsing a new mindset and point of view, moving them from the “taking a pie share” versus the “sharing the pie”.

Entrepreneurs and managers have long been trained, both in theory and in practice, to use a range of techniques first to determine prices for their goods and services, and then to maximize those prices. In almost every industry, the art of “correct (maximized)” pricing is treated as a kind of alchemy: Am I pricing appropriately for this market? Am I leaving value on the table in my transactions? Should I seek higher margins through premium prices aimed at a niche clientele, or lower prices designed to reach a mass market? This dilemma is common, although specific strategies may vary when particular conditions exist, such as constraints on the supply side that make an offer especially attractive to a demand that is not fully satisfied, enabling premium prices to be applied even to large customer segments.

In educational settings and real-world business practice, the factors that facilitate revenue and margin maximization are widely recognized. They include internal elements such as manufacturing and operating costs, which establish the minimum price level required to generate a positive income, as well as external elements such as marketing (for example, brand awareness) and market dynamics (such as the balance between supply and demand, the presence of competitors, and their positioning). These elements form the set of ingredients that enable skilled managers to make complex pricing decisions and to define the market positioning they intend to achieve.

The challenge is different when pricing is designed not only to generate profit, but to secure fair earnings and create value for all stakeholders in the value chain. In this perspective, excellence is reached when margins are used to support the wellbeing of both internal stakeholders (employees, shareholders, collaborators) and external ones (suppliers, customers, service providers). As in the case of profit maximization, there is no universal formula for achieving this broader objective. However, it is possible to rethink how the most common pricing decision factors are used, in order to move toward trade agreements based on fairness, transparency, and recognition of each stakeholder’s contribution. Although this article focuses on B2B transactions, the same principles can and should be applied throughout the entire value chain, up to the end customer.

Withholding versus Sharing Value

A shift toward a more “collective” approach to pricing remains largely a theoretical ambition rather than a concrete operational roadmap, because it requires all supply chain participants to enter negotiations with a different mindset and objectives. In practice, this means aligning buyers and suppliers around shared principles rather than purely individual gains. However, as with any significant change, pioneers must begin somewhere, and in some sectors promising best practices are already emerging.

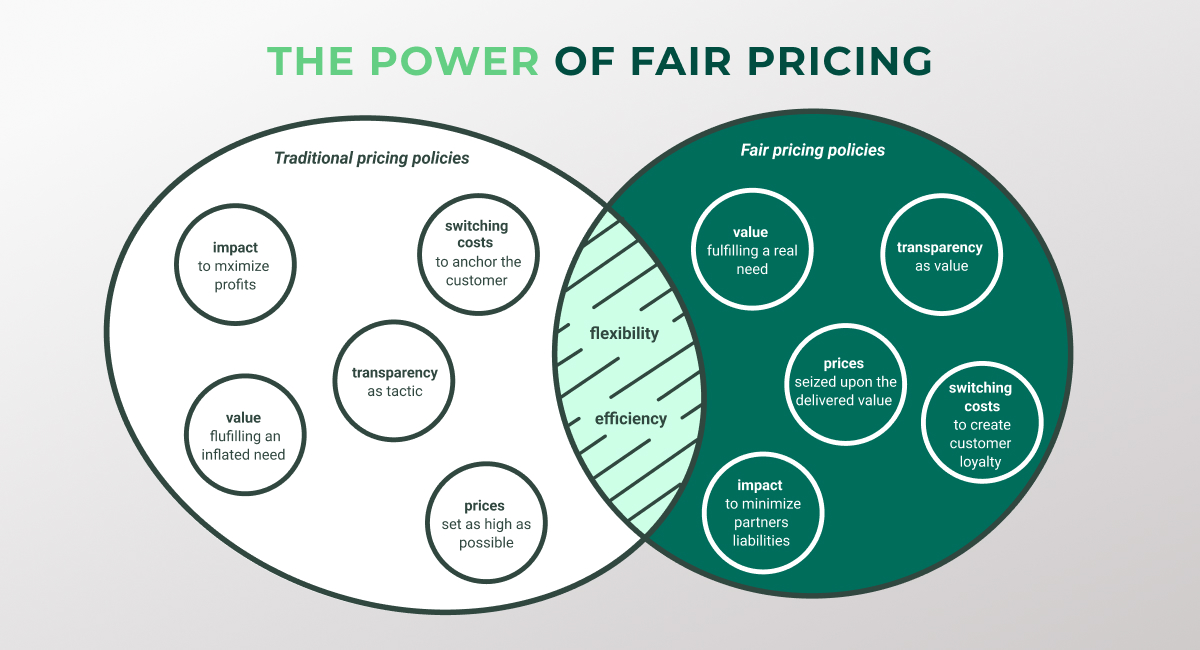

Similar to the broader ESG movement, where meaningful impact depends on the widespread adoption of sustainable practices, fair pricing—an integral component of ESG policies—demands shared values, mutual respect, and a broader evaluation of all stakeholders’ interests. In this context, pricing is not only a financial decision, but also an ethical and strategic one that reflects a company’s commitment to long-term, sustainable relationships. The following table highlights some of the variables managers typically consider when setting prices and shows how, in certain areas, best practices are already in place, while in others a fair-pricing perspective calls for a revised approach grounded in equity and transparency.

The following table outlines key variables that managers typically consider when establishing pricing, noting that best practices are already in use in some areas, while others require a distinct approach aligned with fair pricing principles.

Pricing strategies and elements: a comparable table

| FACTOR | TRADITIONAL PRICING | FAIR PRICING |

| Flexibility | Introducing modular components or options into the offer enhances its

flexibility, allowing it to adapt precisely to the needs of individual customer

segments. Through these deliberate management actions, the company

allocates resources—such as product features and services—to align with

the actual requirements and purchasing power of diverse customer groups.

These qualify as smart actions that optimize resource use, enabling lower

prices scaled to the proposal's scope; both traditional and fair pricing

approaches benefit, as they eliminate unnecessary manufacturing or service

costs that customers neither need nor cannot handle themselves.

Examples within this category include: – Enabling broad product modularity by unbundling features or accessories, letting customers configure their complete package by selecting desired components. – Offering transactional flexibility, such as varied payment terms (e.g., leasing versus outright purchase). – Engaging customers in portions of the process to avoid charging for self-manageable tasks, creating direct savings (e.g., through self- assembly or configuration). |

|

| Value | The value an offer creates for the

customer, by satisfying needs and

providing a product or service that

enables or simplifies a task, should

always be at the core of any

marketing strategy and campaign.

At the same time, companies are

highly skilled at using

complementary marketing actions

to stimulate or even create needs

which, in some categories such as

lifestyle products, can be intangible

or aspirational and therefore often

only partially authentic. Marketers

may argue that if a product fulfils

desires and dreams, it still

generates a positive effect and

delivers on a promise for which

customers are willing to pay, and

this perspective is not necessarily

objectionable, even though in many

cases the value is more “perceived”

than truly “real”.

Under this factor, pricing tends to be set according to demand: the more the product is requested, the more the company marks up its margins. |

Value should be clearly

communicated through concrete facts,

explanations of authentic benefits,

and the specific solutions they provide

to the customer. In addition to listing

positive features, companies should

transparently acknowledge the

limitations of their proposal, fostering

trust through open, fair

communication. This approach builds

stronger customer relationships,

enhances the company’s reputation,

and creates a genuine connection

with the audience.

Whenever feasible, marketers should emphasize tangible benefits and, where appropriate, engage customers psychologically to evoke positive emotions and a sense of wellbeing tied to the purchase or adoption. Pricing should then be determined by objectively assessing the real benefits of the offer compared to alternative market solutions. If the proposal delivers clear savings—whether in money, time, or ease of use—the company can justify a price premium while simultaneously reducing costs for its customers, creating a true win- win scenario. |

| Impact | In practice, sellers should thoroughly understand the impact of their products on their customers' overall supply costs. This insight enables sellers to gauge how much pricing flexibility they have, based on the item's relative importance within the buyer's total purchasing budget. For instance, if a product costs just a few dollars within a multi-million- dollar investment, the seller can apply a higher markup percentage without it being noticed during the buyer's evaluation. | In practice, sellers should thoroughly

understand the impact of their

products on their customers' overall

supply costs. When the product's cost

represents a significant or tangible

portion of that total, sellers must

carefully define the boundaries of fair

margins—going beyond merely

closing the sale to genuinely respect

the buyer's needs and support their

purchasing journey. In fair trade, this

principle works both ways: if price is

not a critical factor for the buyer,

sellers gain flexibility to apply wider

margins, but always within the firm

boundaries of fair pricing ethics. |

| Switching costs | Management doctrine clearly identifies the contextual factors that allow sellers to determine how much they can raise prices without losing the sale—or, more broadly, to maximize profits by selling less volume but increasing overall margins. These variables are collectively known as switching cost factors. They include supply scarcity, product differentiation, availability of alternatives, brand loyalty, and time pressures (such as limited windows in the purchasing process that restrict buyer options). | Fair trade policies view switching

costs from a different perspective.

These factors should always be

maximized and nurtured through good

management practices—creating

demand rigidity remains a wise and

essential goal—but with a focus on

fostering customer loyalty and

retention rather than exploiting them

to raise prices or enhance negotiating

power. For example, in a context of

supply scarcity, even a monopoly

should refrain from extracting extra

profits; instead, it must maintain a fair

mindset by keeping margins at

sustainable, profitable levels without

abusing unbalanced bargaining

power, which also helps attract

potential newcomers who might

otherwise be drawn by inflated market

margins. |

| Efficiency | Pursuing efficiency policies—such as limiting waste and fully exploiting

existing assets—is a fundamental management practice across all types of

companies, regardless of their ultimate strategy. By keeping operating costs

levelled and closely monitored, entrepreneurs can adopt competitive pricing,

conserve resources, and maintain maximum organizational flexibility. For

companies committed to fair pricing, efficiency serves a dual purpose: it not

only strengthens the business but also generates value for the broader

community and its customers. |

|

| Earnings | Companies typically aim to maximize their earnings by

reducing and optimizing costs while

negotiating or setting the highest

prices that a sufficient number of

customers will accept, thereby

accruing profits. On the supply

side, they seek the "best sales

terms" from suppliers and, when

their negotiating power is strong,

often squeeze supplier margins.

These practices can lower

company costs, leading to higher

margins or more competitive end-

customer pricing, but they may also

undermine suppliers' ability to

invest, maintain product quality

over time, or sustain operations.

On the demand side, aggressive pricing, discounts, and promotions are frequently deployed—either because a product is underperforming or poorly positioned, or to capture and defend market share against competitors. |

The company positions itself as both a business and a social actor, with a

mission to create value for all

stakeholders: transforming raw

materials into products or services for

customers, forming alliances with

suppliers to maximize synergies and

improve the shared supply chain,

fostering wellbeing for employees and

local communities, and rewarding

shareholders for their capital and risk.

Such inclusive practices become

feasible when management adopts a

broad perspective, considering each

stakeholder’s viewpoint, needs, and

role in the ecosystem.

The company defines its market positioning and sets pricing that generates fair earnings proportional to the value it creates. Importantly, this does not imply settling for modest profits; earnings should align with the magnitude of value delivered—if the company provides exceptional benefits, it can command higher prices and potentially generate substantial wealth. The emphasis lies not on capping prices, but on capturing value through authentic contributions across the supply chain while maintaining a balanced pricing- to-value ratio. |

| Transparency | Transparency significantly limits opportunities for independent management decisions that maximize margins by exploiting market differences to charge the highest possible prices across channels, segments, and markets. Consequently, pricing is often revealed only after prolonged negotiations, frequently under the pretext of developing a customized solution—even though these variations in features do not always entail genuine cost differences but rather provide sales managers a convenient excuse to finalize pricing after gauging the customer's budget and expectations. | Transparency should be a deliberate

strategic choice for management,

extending beyond mere marketing

tactics. Customers greatly value it,

and a clear pricing policy strengthens

the company’s reputation for reliability

and integrity. At the same time, sellers

must implement it thoughtfully, as any

variable pricing—once

disclosed—requires thorough

explanation and justification, breaking

down cost and revenue components.

Ideally, to establish themselves as authentic market players, companies should present net prices measured their underlying value (avoiding inflated price lists mimicking industry norms where standard quotes include built-in discounts). |

The table effectively illustrates key variables that management should consider transitioning from traditional to fair pricing policies. Companies must first alter their trading behaviour, moving from adversarial negotiations to collaborative efforts that generate joint value; fair pricing is thus part of a broader set of fair management practices that organizations should embrace.

Action Steps

The path forward is straightforward and builds on the principles outlined above: embrace flexibility, pursue efficiency, champion transparency, foster loyalty, and resist the urge to exploit demand rigidity or market segmentation solely to inflate margins based on customer profiles. This shift will not occur overnight, but companies can begin by refining practices in each pricing policy area according to these guidelines.

Overcoming Industry Norms

It demands an innovative mindset that challenges entrenched industry rules—such as doubling list prices only to apply a standard 50% discount because “everyone does it,” or layering on arbitrary reductions like 40% + 5% + 2%, turning pricing into a pointless math exercise. Instead, companies should always quote direct net prices and resist bending to expected negotiations (driven by competitors’ inflated markups), limiting discounts to volume-based incentives where feasible—this fairly accommodates different segments (e.g., a consumer buying one unit versus a distributor ordering 100 for resale) while aligning with the goal of equitable earnings.

Long-Term Benefits

Short-term profit dips during the transition are not necessarily detrimental; they signal a commitment to transparency and fairness, earning customer appreciation, bolstering brand strength, and strengthening competitive positioning—ultimately enabling sustainable premium pricing based on hard-won market trust. Finally, this transformation hinges on mutual adaptation across buyer-seller relationships to a new negotiation culture; if facing an opportunistic partner exploiting your fairness for their gain, persistent education may fail—then decide: walk away or defend your stance

Borello Kingsley Antonio